.svg)

.webp)

.webp)

Source Energy Services Reports Q4 2025 and Year End Results

Calgary, AB

TSX: SHLE

Calgary, Alberta (February 26, 2026) TSX: SHLE

Source Energy Services Ltd. (“Source” or the “Company”) is pleased to announce its financial results for the three and twelve months ended December 31, 2025.

2025 PERFORMANCE HIGHLIGHTS

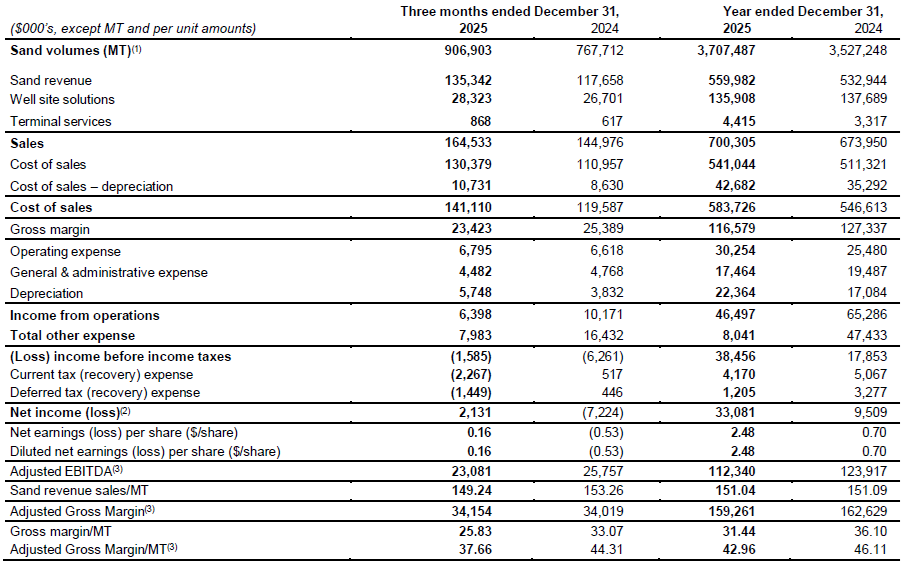

A rebound in activity levels drove volumes of 906,903 metric tonnes (“MT”) for the fourth quarter, an 18% increase over the fourth quarter of 2024, resulting in a record year of volume for Source. For the year ended December 31, 2025, key achievements include the following:

- realized sand sales volumes of 3,707,487 MT and sand revenue of $560.0 million, an increase of $27.0 million or 5% over last year;

- generated total revenue of $700.3 million, a $26.4 million increase over 2024;

- realized gross margin of $116.6 million and Adjusted Gross Margin(1) of $159.3 million, decreases of 8% and 2%, respectively, when compared to last year;

- reported net income of $33.1 million, an increase of $23.6 million over 2024;

- realized Adjusted EBITDA(1) of $112.3 million, an $11.6 million decrease from 2024;

- realized record sand sales volumes and record sand volumes delivered to customer well sites through “last mile” logistics during the first half of the year;

- achieved 74% utilization across the eleven-unit Sahara fleet, compared to 78% last year, as units operating in the US achieved 100% utilization during 2025;

- commenced operations at the Taylor transload facility;

- completed the first phase of the Peace River facility expansion, achieving nameplate domestic sand production capacity of 1,000,000 MT; and

- implemented a Normal Course Issuer Bid program, resulting in the repurchase of 464,800 shares during the year.

Note:

- Adjusted Gross Margin (including on a per MT basis) and Adjusted EBITDA are not defined under IFRS (as defined herein) and might not be comparable to similar financial measures disclosed by other issuers, refer to ‘Non-IFRS Measures’ below for reconciliations to measures recognized by IFRS. For additional information, please refer to Source’s Management’s Discussion and Analysis (“MD&A”), dated February 26, 2026, available online at www.sedarplus.ca.

RESULTS OVERVIEW

Notes:

- One MT is approximately equal to 1.102 short tons.

- The average Canadian to United States (“US”) dollar exchange rate for the three and twelve months ended December 31, 2025, was $0.7170 and $0.7154, respectively (2024 - $0.7152 and $0.7300, respectively).

- Adjusted EBITDA and Adjusted Gross Margin (including on a per MT basis) are not defined under IFRS, refer to ‘Non-IFRS Measures’ below for reconciliations to measures recognized by IFRS. For additional information, please refer to Source’s MD&A available online at www.sedarplus.ca.

2025 Results

Total revenue for the year ended December 31, 2025 was $700.3 million compared to $674.0 million for 2024, an increase of $26.4 million, reflecting strong demand and activity levels realized through most of the year. Despite continued economic uncertainty, which significantly impacted Source customer activity levels during the third quarter, demand rebounded in the fourth quarter as many previously deferred completion jobs were executed. Strong customer activity levels in the Western Canadian Sedimentary Basin (“WCSB”) drove record volumes delivered for “last mile” logistics in 2025, and the three Sahara units operating in the US achieved 100% utilization for the year.

Cost of sales, excluding depreciation, increased for 2025 compared to 2024, driven by record sand sales volumes and higher transportation costs resulting from the increased volumes hauled to the terminals and by “last mile” logistics. Commissioning of the newly expanded Peace River facility was impacted by integration issues with legacy equipment, resulting in incremental costs incurred compared to last year. Cost of sales, excluding depreciation, benefited from lower production costs achieved at the Wisconsin mining facilities. Additional costs associated with Source’s trucking operations and the addition of the Taylor terminal facility also impacted cost of sales, excluding depreciation, compared to 2024. A weakening of the Canadian dollar increased cost of sales denominated in US dollars by $2.54 per MT, compared to 2024, which was largely offset by the movement in exchange rates on revenue denominated in US dollars for the year.

For the year ended December 31, 2025, gross margin decreased by $10.8 million compared to 2024. Excluding margin from mine gate volumes, Adjusted Gross Margin was $43.71 per MT compared to $46.99 per MT in 2024, impacted by a shift in terminal and product mix and incremental costs incurred for the Peace River facility expansion, as noted above. These impacts were partially offset by $3.6 million of incremental margin generated from Source’s trucking operations and lower rail transportation costs realized late in 2025. Adjusted Gross Margin also reflects higher costs related to expanded terminal facility operations, including the commencement of operations at the Taylor terminal facility, compared to 2024. The weakening of the Canadian dollar negatively impacted Adjusted Gross Margin by $0.24 per MT for 2025, compared to last year.

Operating expense increased by $4.8 million on a year-over-year basis, largely driven by higher royalty-related costs, increased compensation expense, including incremental people costs for trucking and terminal operations, and higher rail car-related expenses. General and administrative expense decreased by $2.0 million compared to 2024 due primarily to lower people costs, driven by lower variable incentive compensation expense, partly offset by an increase in IT costs, attributed to the cloud-computing system implemented last year, and higher costs for professional fees.

Adjusted EBITDA decreased by 9%, or $11.6 million, to $112.3 million for the year ended December 31, 2025. The reduction is mainly attributed to a significant slowdown in Source customer activity levels experienced during the third quarter, as noted above, an increase in finer mesh sand sales and incremental costs incurred at the Peace River mining facility. Last year, Adjusted EBITDA benefited by $3.9 million from the commencement of the leases for Source’s tenth and eleventh Sahara units. Despite a weakening of the Canadian dollar compared to last year, Adjusted EBITDA was not impacted, largely attributed to the movement in exchange rates on the repayment of long-term debt.

Liquidity and Capital Resources

Notes:

- Adjusted EBITDA and Free Cash Flow are not defined under IFRS and might not be comparable to similar financial measures disclosed by other issuers, refer to ‘Non-IFRS Measures’ below. The reconciliation to the comparable IFRS measure can be found in the table below.

- Excludes capital expenditures for the Taylor facility.

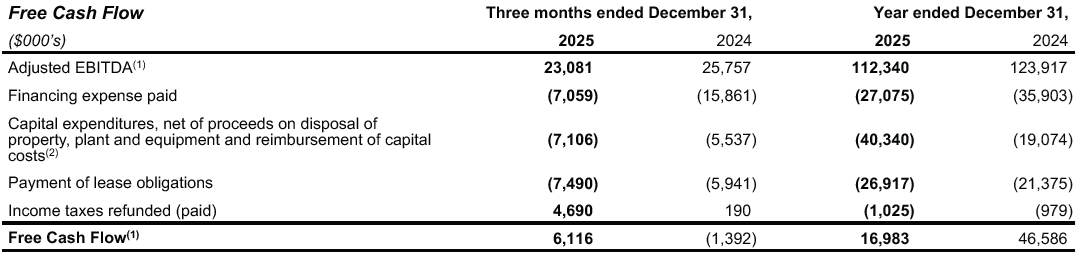

Source generated Free Cash Flow of $6.1 million for the fourth quarter of 2025, an increase of $7.5 million compared to the fourth quarter of 2024. The increase was mainly due to lower financing expenses paid and refunded income taxes. During the fourth quarter of 2024, Source incurred finance expenses associated with the refinancing of its credit facilities in December 2024. For the fourth quarter of 2025, Free Cash Flow was impacted by higher amounts for capital expenditures of $1.6 million, primarily due to expansion at the Peace River facility, and higher amounts paid for lease obligations, resulting from additional heavy equipment at Peace River and higher lease rate renewals for Wisconsin mining operations.

On a year-to-date basis, Free Cash Flow decreased by $29.6 million compared to 2024, largely attributed to higher capital expenditures related to the Peace River facility expansion and sand processing assets purchased during the third quarter. Free Cash Flow was also impacted by a slowdown in activity levels during the third quarter of 2025, as Source customers deferred certain projects into late 2025 and early 2026. Additional heavy equipment for mining operations in Canada and higher renewal rates for US operations increased amounts paid for lease obligations compared to 2024.

Capital expenditures, net of proceeds on disposals and reimbursements and excluding expenditures related to the Taylor facility, were $7.1 million for the three months ended December 31, 2025, an increase of $1.6 million compared to the fourth quarter last year. Excluding proceeds on disposal and reimbursements and construction for the Taylor facility, growth capital expenditures increased by $2.1 million, mainly attributed to expansion at the Peace River facility. During the fourth quarter of 2024, a customer reimbursement related to the Peace River facility expansion lowered total expenditures incurred during the quarter, offsetting amounts spent for the Chetwynd terminal expansion and costs to complete Source’s eleventh Sahara unit. Maintenance and sustaining capital expenditures decreased by $0.5 million for the fourth quarter of 2025, compared to the same period last year, driven by lower amounts incurred for facility improvements, partly offset by amounts incurred for Source’s trucking operations and various small upgrade projects at the Wisconsin mining facilities.

During the year ended December 31, 2025, capital expenditures, net of proceeds on disposals and reimbursements and excluding expenditures related to the Taylor facility, increased by $21.3 million compared to 2024. Excluding expenditures for the Taylor facility and proceeds on disposal and reimbursements, growth capital expenditures increased by $15.7 million, primarily due to the Peace River assets acquired during the third quarter and expansion at the existing Peace River facility, with the current phase of the expansion to 1,000,000 MT of domestic sand production now complete. Expenditures for sustaining capital increased by $5.5 million for 2025 compared to last year, driven by higher amounts for overburden removal and increased expenditures for Sahara improvements and upgrades, as well as equipment rebuilds for Source’s trucking operations.

Q4 2025 RESULTS

For the three months ended December 31, 2025, Source generated sand sales volumes of 906,903 MT, an 18% increase over the fourth quarter of 2024, and sand revenue of $135.3 million, a $17.7 million increase over the same period in 2024. The increase was primarily driven by a rebound in Source customer activity levels, as several customers deferred third quarter work into the fourth quarter and early 2026. Average realized sand price decreased by $4.02 per MT compared to the same period last year, attributed to a shift in product mix and the impact of lower-priced, finer mesh sand sales. The increased proportion of lower-value sand volumes contributes to a more balanced mesh demand profile which supports improved production efficiency and higher processing yields.

Well site solutions revenue totaled $28.3 million for the fourth quarter of 2025, an increase of $1.6 million or 6% compared to the fourth quarter of 2024. This increase was driven by higher volumes delivered by “last mile” logistics, reflecting strong Source customer activity levels and longer trips to well sites compared to the same period in 2024. Sahara units in Canada were 50% utilized during the fourth quarter, a 4% increase compared to fourth quarter of 2024, and Sahara units deployed in the US remained fully contracted, maintaining 100% utilization during the quarter. For the fourth quarter of 2025, terminal services revenue increased by $0.3 million compared to the fourth quarter of 2024, due to an increase in revenue from higher chemical elevation volumes realized, as well as sand elevation storage rate increases.

Cost of sales, excluding depreciation, increased by $19.4 million for the three months ended December 31, 2025 compared to the fourth quarter of 2024, driven by higher sand volumes sold and incremental costs incurred for the Peace River facility in 2025. Commissioning of the newly expanded facility was impacted by integration issues with legacy equipment, resulting in incremental costs incurred. The increase in overall cost of sales also reflects higher people costs and higher repairs and maintenance expenses for equipment, largely attributed to the sand trucking assets purchased last year, as well as incremental royalty costs for the Peace River facility, driven by increased production levels. Compared to the fourth quarter of 2024, a reduction in third party trucking costs favorably impacted cost of sales, excluding depreciation, driving lower costs for transportation. On a per tonne basis, cost of sales, excluding depreciation was impacted by a shift in terminal mix, partly offset by lower costs for rail-related transportation during the quarter. The impact of the movement in foreign exchange rates on US dollar denominated components of cost of sales drove a decrease of $0.25 per MT to cost of sales, excluding depreciation, compared to the fourth quarter last year.

Gross margin decreased by $2.0 million and Adjusted Gross Margin improved by $0.1 million for the three months ended December 31, 2025, attributed to the increase in activity levels realized during the period. Excluding gross margin from mine gate volumes, Adjusted Gross Margin was $39.07 per MT, compared to $44.88 per MT for the fourth quarter of 2024. The fourth quarter was impacted by incremental costs at the Peace River facility, as noted above, as well as extremely cold temperatures and heavy snowfall in certain Source customer operating areas, resulting in additional performance-related charges which impacted Adjusted Gross Margin by $0.52 per MT. For the three months ended December 31, 2025, the strengthening of the Canadian dollar led to a decrease of Adjusted Gross Margin by approximately $0.02 per MT.

For the fourth quarter of 2025, total operating and general and administrative expense decreased by $0.1 million compared to the same period of 2024. Operating expense increased by $0.2 million, mainly due to higher selling and administrative costs, including higher royalty expenses, increased workers’ compensation premiums and property tax expenses. These cost pressures were partially offset by lower people costs, reflecting reduced incentive compensation expense compared to the fourth quarter last year.

General and administrative expense decreased by $0.3 million for the three months ended December 31, 2025, primarily due to lower people costs, reflecting lower incentive compensation expense, and a reduction in IT related expenses. During the fourth quarter of 2024, Source implemented a new cloud-computing software system which resulted in incremental expenses incurred during the period. An increase in costs for legal fees partly offset the reductions in general and administrative expense, compared to the same period in 2024.

BUSINESS OUTLOOK

Source anticipates most customers will adopt a more defensive budget approach for 2026, a reflection of the current commodity price environment. As a result, Source expects 2026 customer activity levels to be broadly consistent with 2025 activity levels. While higher commodity prices could provide upside to expected volumes for 2026, over the medium to longer term, the Western Canadian LNG projects currently being constructed, along with the expedited permitting of additional LNG capacity, including the recent approval of the KSI Lisims project by the government of British Columbia and the inclusion of LNG Canada (Phase 2) in the Government of Canada’s major projects list, will drive incremental demand for proppant in the WCSB. Source believes it is well-positioned to capitalize on the expected demand increase in northeastern British Columbia and to take advantage of growing proppant demand levels in the WCSB through its existing northern white sand franchise, expanded terminal network and growing domestic sand production at Peace River.

Source believes the increased demand for natural gas, driven by liquefied natural gas exports, increased natural gas pipeline export capabilities and power generation facilities, will drive incremental demand for Source’s services in the WCSB. Source continues to see increased demand from customers that are primarily focused on the development of natural gas properties in the Montney, Duvernay and Deep Basin.

Source also continues to focus on increasing its involvement in the provision of logistics services for other items needed at the well site in response to customer requests to expand its service offerings and to further utilize its existing Western Canadian terminals to provide additional services.

UPDATED NI 43-101 TECHNICAL REPORTS FOR THE MINERAL PROJECTS IN WISCONSIN, UNITED STATES

Source is pleased to announce that it has filed with the applicable Canadian securities regulatory authorities updated National Instrument 43-101 – Standards of Disclosure for Mineral Projects (“NI 43-101”) technical reports for each of its three mineral projects in Wisconsin, United States (collectively, the “Technical Reports”).

The Technical Reports have each been prepared with an effective date of December 31, 2025 and were updated as part of an annual assessment that accounts for conventional mining depletion of the mineral resources and include updated production records. The updated resources do not represent a 100% or greater change in the total mineral resources.

Mineral resources are not mineral reserves and do not have demonstrated economic viability. There is no guarantee that all or any part of the mineral resource will be converted into a mineral reserve. Source has not based its production decisions and ongoing mine production on mineral reserve estimates, preliminary economic assessments, prefeasibility studies or feasibility studies. As a result, there may be an increased uncertainty of achieving any particular level of recovery of minerals or the cost of such recovery and historical projects without any mineral reserves have increased uncertainty and risk of failure.

Further details with respect to the scientific and technical information contained in this press release are available in the Technical Reports, which are available under the Company’s SEDAR+ profile at www.sedarplus.ca.

FOURTH QUARTER CONFERENCE CALL

A conference call to discuss Source’s fourth quarter financial results has been scheduled for 7:30 am MST (9:30 am ET) on Friday, February 27, 2026.

Interested analysts, investors and media representatives are invited to register to participate in the call. Once you are registered, a dial-in number and passcode will be provided to you via email. The link to register for the call is on the Upcoming Events page of our website and as follows:

Source Energy Services Q4 2025 Results Call

The call will be recorded and available for playback approximately 2 hours after the meeting end time, until March 27, 2026, using the following dial-in:

Toll-Free Playback Number: 1-855-669-9658

Playback Passcode: 6972398

ABOUT SOURCE ENERGY SERVICES

Source is a company that focuses on the integrated production and distribution of frac sand, as well as the distribution of other bulk completion materials not produced by Source. Source provides its customers with an end-to-end solution for frac sand supported by its Wisconsin and Peace River mines and processing facilities, its Western Canadian terminal network and its “last mile” logistics capabilities, including its trucking operations, and Sahara, a proprietary well site mobile sand storage and handling system.

Source’s full-service approach allows customers to rely on its logistics platform to increase reliability of supply and to ensure the timely delivery of frac sand and other bulk completion materials at the well site.

IMPORTANT INFORMATION

These results should be read in conjunction with Source’s audited consolidated financial statements for the years ended December 31, 2025 and 2024, together with the accompanying notes (the “Financial Statements”) and its corresponding MD&A for such periods. The Financial Statements and MD&A and other information relating to Source, including the Annual Information Form, are available under the Company’s SEDAR+ profile at www.sedarplus.ca. The Financial Statements and comparative statements have been prepared in accordance with International Financial Reporting Standards (“IFRS”) as issued by the International Accounting Standards Board. Unless otherwise stated, all amounts are expressed in Canadian dollars.

NON-IFRS MEASURES

In this press release Source has used the terms Free Cash Flow, Adjusted Gross Margin and Adjusted EBITDA, including per MT, which do not have standardized meanings prescribed by IFRS and Source’s method of calculating these measures may differ from the method used by other entities and, accordingly, they may not be comparable to similar measures presented by other companies. These financial measures should not be considered as an alternative to, or more meaningful than, net income and gross margin, respectively, which represent the most directly comparable measures of financial performance as determined in accordance with IFRS.

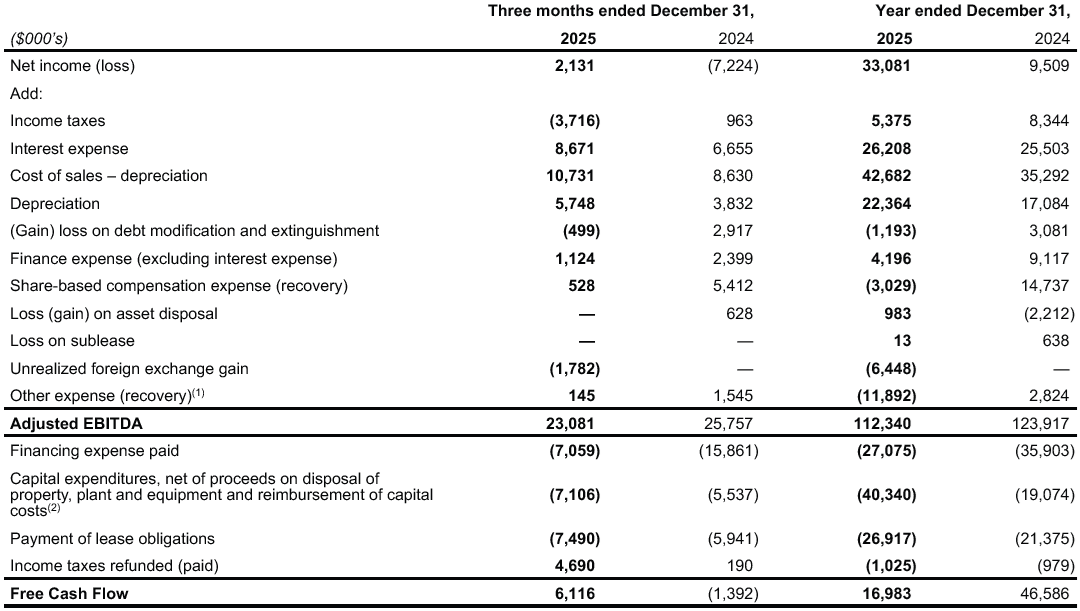

Reconciliation of Adjusted EBITDA and Free Cash Flow to Net Income (Loss)

Notes:

- Includes expenses and recoveries related to the incident at the Fox Creek terminal facility, costs and reimbursements under insurance claims and other one-time expenses.

- Excludes capital expenditures for the Taylor facility.

Reconciliation of Gross Margin to Adjusted Gross Margin

For additional information regarding non-IFRS measures, including their use to management and investors, their composition and discussion of changes to either their composition or label, if any, please refer to the ‘Non-IFRS Measures’ section of the MD&A, which is incorporated herein by reference. Source’s MD&A is available online at www.sedarplus.ca and through Source’s website at www.sourceenergyservices.com.

FORWARD-LOOKING STATEMENTS

Certain statements contained in this press release constitute forward-looking statements relating to, without limitation, expectations, intentions, plans and beliefs, including information as to the future events, results of operations and Source’s future performance (both operational and financial) and business prospects. In certain cases, forward-looking statements can be identified by the use of words such as “approach”, “anticipates”, “expects”, “believes”, “continues”, “focus”, “could”, “improve” or variations of such words and phrases, or statements that certain actions, events or results “may” or “will” be taken, occur or be achieved. Such forward-looking statements reflect Source’s beliefs, estimates and opinions regarding its future growth, results of operations, future performance (both operational and financial), and business prospects and opportunities at the time such statements are made, and Source undertakes no obligation to update forward-looking statements if these beliefs, estimates and opinions or circumstances should change unless required by applicable law. Forward-looking statements are necessarily based upon a number of estimates and assumptions made by Source that are inherently subject to significant business, economic, competitive, political and social uncertainties and contingencies. Forward-looking statements are not guarantees of future performance.

In particular, this press release contains forward-looking statements pertaining, but not limited to: Source’s continued focus on the integrated production and distribution of frac sand and the distribution of other bulk completion materials not produced by Source; Source’s full-service approach which allows customers to rely on its logistics platform to increase reliability of supply and to ensure the timely delivery of frac sand and other bulk completion materials at the well site; expectation that customers will adopt a more defensive budget approach for 2026; robust proppant demand in 2026; the expectation that Western Canadian LNG projects will drive incremental demand for proppant in the WCSB; the belief that Source is well-positioned to capitalize on the increase in demand in northeastern British Columbia and take advantage of growing activity levels in the WCSB; belief that 2026 customer activity levels are to be broadly consistent with 2025 activity levels; expectations with respect to sand revenue and mine gate sand sales and associated costs; expectations that increased demand for natural gas, increased natural gas pipeline export capabilities and liquefied natural gas exports will drive incremental demand for Source’s services in the WCSB; expectations regarding the continuing expansion of the Peace River mining facility; continued increase in demand from customers primarily focused on the development of natural gas properties in Montney, Duvernay and Deep Basin; Source’s focus on and expectations regarding increasing its involvement in the provision of logistics services for other well site items; the benefits of Source’s existing Western Canadian terminals to provide additional services to customers; the benefits that Source’s “last mile” services provide to customers; expectations respecting future conditions; and profitability.

By their nature, forward-looking statements involve numerous current assumptions, known and unknown risks, uncertainties and other factors which may cause the actual results, performance or achievements of Source to differ materially from those anticipated by Source and described in the forward-looking statements.

With respect to the forward-looking statements contained in this press release, assumptions have been made regarding, among other things: proppant market prices; future oil, natural gas and liquefied natural gas prices; future global economic and financial conditions, including the results of ongoing tariff and trade negotiations in North America, as well as globally; predictable inflationary pressures; future commodity prices, demand for oil and gas and the product mix of such demand; levels of activity in the oil and gas industry in the areas in which Source operates; the continued availability of timely and safe transportation for Source’s products, including without limitation, Source’s rail car fleet and the accessibility of additional transportation by rail and truck; the maintenance of Source’s key customers and the financial strength of its key customers; the maintenance of Source’s significant contracts or their replacement with new contracts on substantially similar terms and that contractual counterparties will comply with current contractual terms; operating costs; that the regulatory environment in which Source operates will be maintained in the manner currently anticipated by Source; future exchange and interest rates; geological and engineering estimates in respect of Source’s resources; the recoverability of Source’s resources; the accuracy and veracity of information and projections sourced from third parties respecting, among other things, future industry conditions and product demand; demand for horizontal drilling and hydraulic fracturing and the maintenance of current techniques and procedures, particularly with respect to the use of proppants; Source’s ability to obtain qualified staff and equipment in a timely and cost-efficient manner; Source’s ability to maintain their information assets and critical infrastructure and cyber security; impacts of U.S. legislation and regulatory policies; the regulatory framework governing royalties, taxes and environmental matters in the jurisdictions in which Source conducts its business and any other jurisdictions in which Source may conduct its business in the future; future capital expenditures to be made by Source; future sources of funding for Source’s capital program; Source’s future debt levels; the impact of competition on Source; and Source’s ability to obtain financing on acceptable terms.

A number of factors, risks and uncertainties could cause results to differ materially from those anticipated and described herein including, among others: the effects of competition and pricing pressures; risks inherent in key customer dependence; effects of fluctuations in the price of proppants; risks related to indebtedness and liquidity, including Source’s leverage, restrictive covenants in Source’s debt instruments and Source’s capital requirements; risks related to interest rate fluctuations and foreign exchange rate fluctuations; changes in general economic, financial, market and business conditions in the markets in which Source operates, including with respect to tariff and trade policy in North America, as well as globally; changes in the technologies used to drill for and produce oil and natural gas; Source’s ability to obtain, maintain and renew required permits, licenses and approvals from regulatory authorities; the stringent requirements of and potential changes to applicable legislation, regulations and standards; the ability of Source to comply with unexpected costs of government regulations; liabilities resulting from Source’s operations; the results of litigation or regulatory proceedings that may be brought by or against Source; the ability of Source to successfully bid on new contracts and the loss of significant contracts; uninsured and underinsured losses; risks related to the transportation of Source’s products, including potential rail line interruptions or a reduction in rail car availability; the geographic and customer concentration of Source; the impact of extreme weather patterns and natural disasters; the impact of climate change risk; the ability of Source to retain and attract qualified management and staff in the markets in which Source operates; labor disputes and work stoppages and risks related to employee health and safety; general risks associated with the oil and natural gas industry, loss of markets, consumer and business spending and borrowing trends; limited, unfavorable, or a lack of access to capital markets; uncertainties inherent in estimating quantities of mineral resources; sand processing problems; implementation of recently issued accounting standards; the use and suitability of Source’s accounting estimates and judgments; the impact of information systems and cyber security breaches; the impact of inflation on capital expenditures; and risks and uncertainties related to pandemics, including changes in energy demand.

Although Source has attempted to identify important factors that could cause actual actions, events or results to differ materially from those described in the forward-looking statements, there may be other factors that cause actions, events or results not to be as anticipated, estimated or intended. There can be no assurance that forward-looking statements will materialize or prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. The forward-looking statements contained in this press release are expressly qualified by this cautionary statement. Readers should not place undue reliance on forward-looking statements. These statements speak only as of the date of this press release. Except as may be required by law, Source expressly disclaims any intention or obligation to revise or update any forward-looking statements or information whether as a result of new information, future events or otherwise.

Any financial outlook and future-oriented financial information contained in this press release regarding prospective financial performance, financial position or cash flows is based on assumptions about future events, including economic conditions and proposed courses of action based on management’s assessment of the relevant information that is currently available. Projected operational information contains forward-looking information and is based on a number of material assumptions and factors, as are set out above. These projections may also be considered to contain future oriented financial information or a financial outlook. The actual results of Source’s operations for any period will likely vary from the amounts set forth in these projections and such variations may be material. Actual results will vary from projected results. Readers are cautioned that any such financial outlook and future-oriented financial information contained herein should not be used for purposes other than those for which it is disclosed herein. The forward-looking information and statements contained in this document speak only as of the date hereof and have been approved by the Company’s management as at the date hereof. The Company does not assume any obligation to publicly update or revise them to reflect new events or circumstances, except as may be required pursuant to applicable laws.